While the highly inflated value of the U.S. Retirement Market reached a new high this year, something is seriously wrong when we look behind the scenes. Of course, Americans have no idea that the U.S. Retirement Market is only a few steps from falling off the cliff because their eyes are focused on the shiny spinning roulette wheel called the Wall Street Stock Market.

Yes, everyone continues to place their bets, hoping and praying that they will win it big, so they can retire in style. Unfortunately, American gamblers at the casino have no idea that the HOUSE is out of money. The only thing remaining in their backroom vaults is a small stash of cash and a bunch of IOUs and debts.

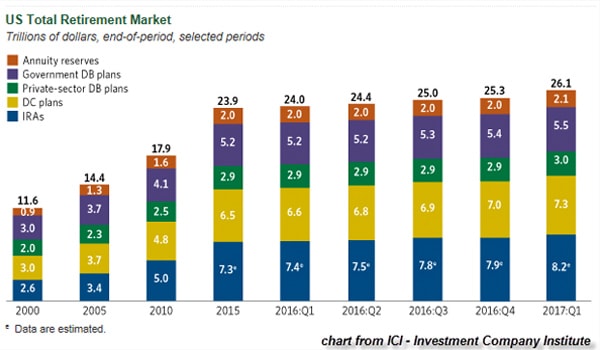

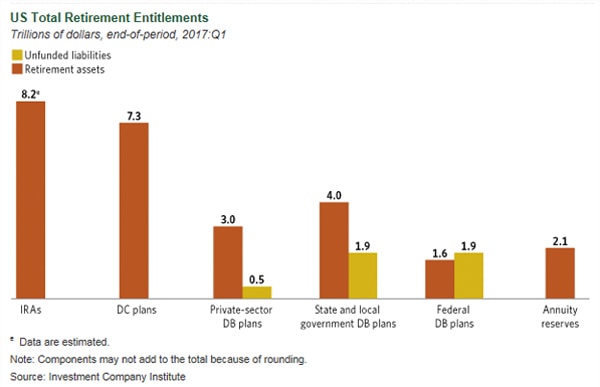

According to the ICI – Investment Company Institute, the U.S. Retirement Market hit a new record $26.1 trillion in the first quarter of 2017:

This New Record High in U.S. Retirement Assets

It is most certainly a good moral booster for Americans. As their retirement assets continue to increase, this provides them a wonderful incentive to fork over more of their hard-earned monthly income to feed the DARK HOLE I label the U.S. Retirement PAC-MAN Monster.

Regrettably, Americans have no idea that their monthly retirement contributions are not being saved or stored in a nice gold vault, rather they are being used to pay the lucky slobs who retired before them. Now, when I say SLOBS or POOR SLOBS, I am not being derogatory. However, I am using the word as a Wall Street Banker would label those they prey upon.

Regardless, as the U.S. Retirement Market continued higher over the past several years, the amount of net contributions has gone into negative territory. As I have mentioned before, this is a beginning sign of a Ponzi Scheme in its last stages. In my previous article, WARNING: U.S. Ponzi Retirement Market In Big Trouble, Protect With Precious Metals, I posted the following chart:

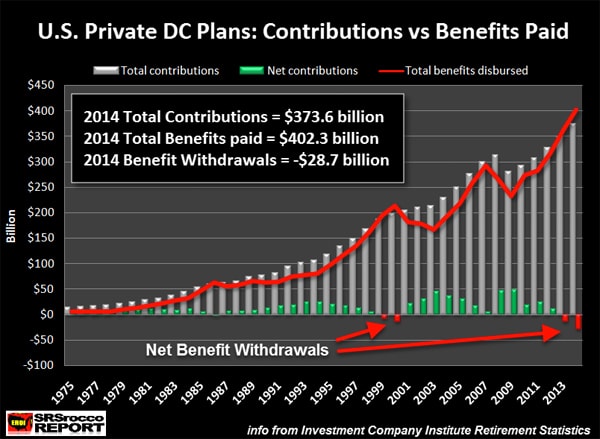

As we can see in the chart, the Private Defined Contribution (DC) Plans paid out $28.7 billion more than they took in 2014…. the last year the Investment Company Institute provided data. Simply, Private DC Plans are mostly 401K’s. If we look up at the first chart with the colorful breakdown of the different U.S. Retirement Plans, DC Plans (mostly 401K’s shown in YELLOW) were valued at $7.3 trillion.

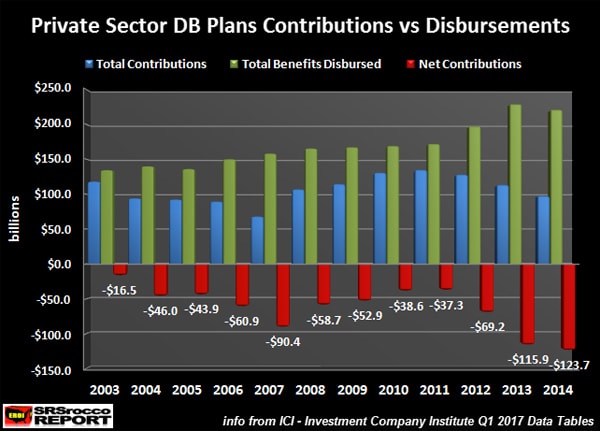

To see U.S. DC plans now paying out more than they receive is certainly bad news… but it isn’t as bad as what is taking place in the U.S. DB – Defined Benefit Plan market. A Defined Benefit Plan is where an employer pays the employee a specific pension payment, based on the employees earning history.

If we look at the U.S. Private DC Plan chart below, we can see what a serious mess it is in:

The GREEN BARS show how much is paid out to retired employees, the BLUE BARS are what is contributed to the DB Plan, and the RED BARS denote how much more is going out than coming in. It doesn’t take much of a brain surgeon to figure out this is not sustainable.

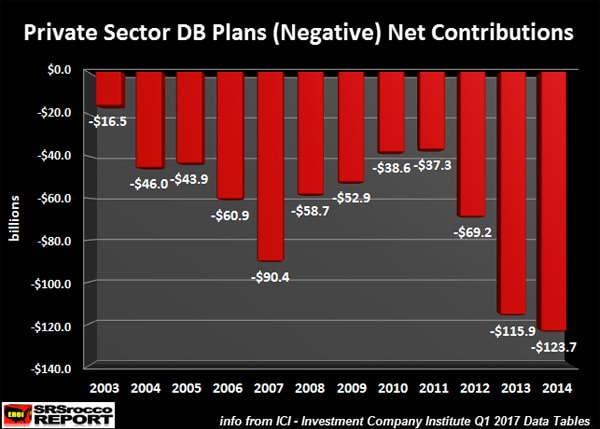

To get a better look at how much RED is going on the U.S. Private Sector DB Plan, I presented the figures in the chart below:

As of the last year the Investment Company Institute published the figures (2014), $123.7 billion more was paid out to employees in the Private Sector DB Plan than came in. While larger payouts have been going out than funds coming in for quite some time, they have also reached a new RECORD HIGH. Ain’t records great?

Okay… let’s bring back the first chart with all the wonderful colors:

The Private Sector DB Plan is shown in the nice GREEN COLOR above at $3 trillion in assets. Again, these are from the Private Sector. If we look at the Government DB Plans in PURPLE, they are valued at $5.5 trillion. Unfortunately, the Government DB Plans (State & Federal) Pension Plans are in much worse shape than the Private Sector DB Plans.

How much worse? Look at the chart below:

The Private Sector DB Plans are underfunded by $500 billion, while the Federal and State-Local DB Plans are underfunded by $3.8 trillion (adding columns together). Even more amusing is that the Federal DB Pension Plans hold a larger underfunded liability than their total assets. While we have heard in the news that the State Pension Plans are in big trouble, we can see the Federal Govt Pension Plans are in much worse shape… LOL.

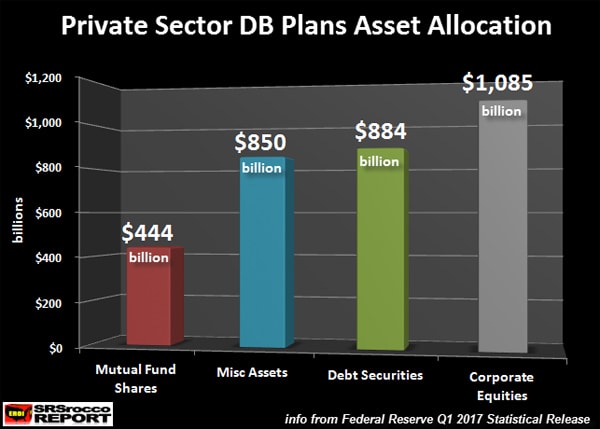

That being said, the U.S. Retirement Market is filled with assets that are based on highly inflated values. I took a look at the Federal Reserve Board of Governors Q1 2017 Statistical Review and listed the top Private Sector DB Plans assets in the chart below:

Of the $3 Trillion in Total Private Sector DB Plan Assets

Corporate Equities (stocks) are valued at $1,085 billion ($1.08 trillion), Debt Securities are $884 billion, Misc Assets are $850 billion and Mutual Fund Shares are $444 billion. Here are my comments on the figures above:

FIRST... If our eyes are not glued to the TV watching CNBC, we should be able to realize that stocks are highly inflated via their extremely bloated P/E – Price to Earnings ratio. So, that $1.08 trillion of Corporate Equities will most certainly collapse in value in the future. This is bad news for both the poor slobs who have been paying in for decades and those retirees who were counting on that monthly income to pay for their $250,000 RV Motor Coach.

SECOND... I find it extremely hilarious that “Debt Securities” valued at $884 billion, can be labeled as “Assets.” Yes, I realize that U.S. Treasuries and Foreign Bonds have been assets in the past, but where we are heading… supposed assets will turn into liabilities, quite quickly.

THIRD.... $844 billion in Misc Assets are not something I would feel comfortable being invested in. Sure, I could see possibly $20-$50 billion in Misc Assets, but $884 billion? This reminds me of Misc chicken parts used to make Mcdonald's high-quality Chicken Nuggets.

FOURTH... Mutual Funds are worse than plain ole stocks… if you ask me. Mutual Funds are claims on claims on stocks. So, this segment of the U.S. Private Sector DB Plan will turn into vapor quicker than most when a fan hits the bull excrement.

While the bloated $3 trillion Private Sector DB Plan Assets are only a small portion of the U.S. Retirement Market, we can assume the disease has spread throughout the entire $26.1 trillion market.

Lastly, it took me a while to come to this conclusion, but I now realize why the Fed and Central Banks pushed all that PHAT QE Money into Stocks, Bonds, and Real Estate. If we are already seeing many sectors of the U.S. Retirement Market paying out more funds than are coming in… what in the living HELL does the U.S. Retirement Market look like when Stock, Bond, and Real Estate values plummet?

That’s right..... it’s going to be BIG, BAD & UGLY.

About the Author:

Independent researcher Steve St. Angelo started to invest in precious metals in 2002. In 2008, he began researching areas of the gold and silver market that the majority of the precious metal analyst community has left unexplored. These areas include how energy and the falling EROI – Energy Returned On Invested – stand to impact the mining industry, precious metals, paper assets, and the overall economy.