Silver mine supply from the world’s fourth-largest silver producer fell significantly at the beginning of 2018. According to Chile’s Ministry of Mines, domestic silver production in January declined 20% versus the same month last year. Chile’s silver production has been falling considerably since its recent peak in 2014.

In just three years, Chile’s domestic silver mine supply fell 10 million oz (Moz) from 50.1 Moz in 2014 to 40.4 Moz last year. Interestingly, Chile’s silver production is down 20% since 2014 while the country’s copper mine supply is only down 5%. Because most of Chile’s silver supply comes as a by-product of copper mining, it’s surprising to see such a significant decline in their silver production.

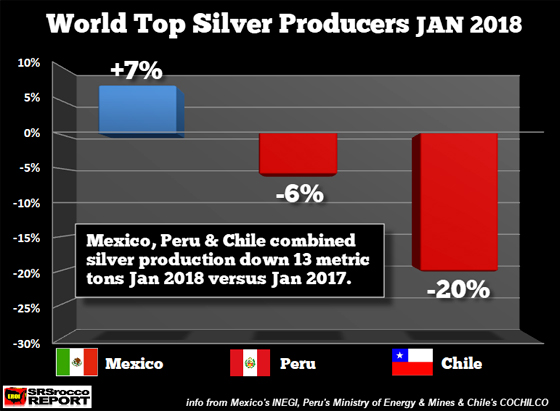

If we look at three of the top four silver producers in the world, Mexico’s silver mine supply in January increased by 7% while Peru declined by 6%:

According to the official data, Mexico’s silver production increased by 29 metric tons (mt), Peru fell by 20 mt and Chile dropped by nearly 21 mt. Thus, overall silver mine supply from these top three producers fell 13 mt in January versus the same month last year. Even though Mexico will likely experience an increase in silver mine supply in 2018, declining production from other leading countries may curtail overall world supply.

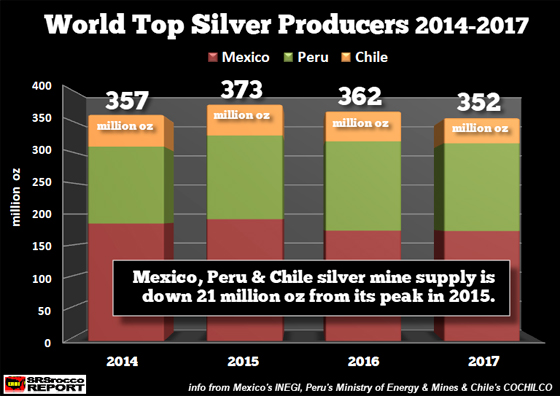

If we look at total silver production from these three countries, the peak took place in 2015 at 373 million oz:

In just two years, the combined silver output from Mexico, Peru, and Chile is down 21 Moz. Now, what’s even more interesting is the growing disparity in production figures released by the official governments and those collected by Thomson Reuters GFMS and published in the World Silver Surveys.

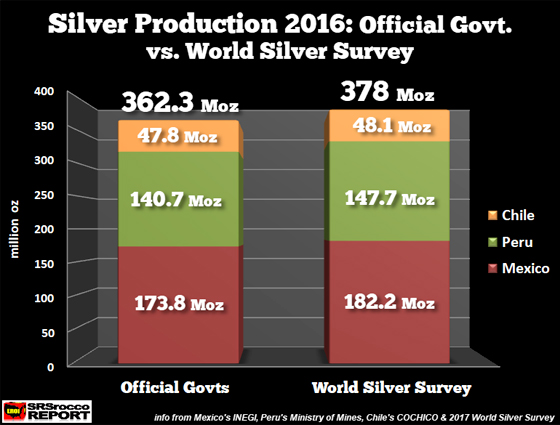

For example, the official government sources report that the combined silver production in 2016 from Mexico, Peru, and Chile was 362.3 Moz versus 378 Moz published in the World Silver Survey:

As we can see, the World Silver Survey stated a total of nearly 16 Moz more in silver production than what was reported by the data from three official governments. When I look at the previous mine supply data published in the World Silver Survey, it was very close to the same figures reported by the official government data. However, over the past few years, the World Silver Survey’s silver production figures for several countries were higher than the data put out by government sources.

Now, there isn’t an advantage for these governments to understate production. We must remember, these governments receive royalties payments and taxes from domestic mine production. So, for whatever reason, that data in the World Silver Survey shows an additional 16 Moz versus what these governments are reporting. If the government sources are more accurate, then the World Silver Survey’s total of 886 Moz published for 2016, is more like 870 Moz.

Now, this is quite interesting because the preliminary mine supply figures published in the Nov 2017 Silver Interim Report, show world silver production of 886 Moz in 2016 will decline to 870 Moz in 2017. According to the data from the 2017 Interim Report, the decline in world silver production was due to significant decreases coming from Chile, Australia, and Guatemala. Well, if world silver production was closer to 870 Moz in 2016, and we include the declines from those three countries then the forecasted global total for 2017 should be approximately 850 Moz.

Lastly, even though we may see an increase in silver production from Mexico, overall global mine supply will likely start to decline more rapidly over the next several years. Why? A stock market meltdown will destroy demand for base metals and the silver supply as a by-product of copper, lead, and zinc production.

A falling mine supply of silver when investors around the world wake up to the tremendous STORE OF WEALTH properties of the poor man’s gold should do wonders for its value in the future.

About the Author:

Independent researcher Steve St. Angelo started to invest in precious metals in 2002. In 2008, he began researching areas of the gold and silver market that the majority of the precious metal analyst community has left unexplored. These areas include how energy and the falling EROI – Energy Returned On Invested – stand to impact the mining industry, precious metals, paper assets, and the overall economy.